NameSilo Technologies -- Investment Thesis

Reinvesting free cash flows from the web domain business into new businesses drives the investment case

This document is a work in progress. Come back later if you’d like to see the completed document. Please comment if you have any questions or corrections! This is for information only and is not financial advice, nor am I your investment advisor. (ticker $URL.CN, C$1.51; OTC $URLOF, US$1.10)

NameSilo Technologies is a Canadian-domiciled holding company which primarily reinvests the free cash flow from its 81.5%-owned operating company, NameSilo LLC, one of the world’s 10 largest web domain hosts. NameSilo LLC does not require a lot of reinvestment to maintain the business, and there isn’t much opportunity to reinvest the cash flow profitably into growing the web domain business. Therefore, the parent company is structured to reinvest the cash flow into other opportunities. Fortunately, the NameSilo Technologies’ CEO is an excellent capital allocator as an outstanding investor in Canadian microcap stocks.

The primary components of the parent company NameSilo Technologies’ value are:

1. The web domain operating business, NameSilo LLC, 81.5% owned by the parent company, which provides steady free cash flow for other investments;

2. The reinvestment runway provided by a seasoned team of microcap investors, including CEO Paul Andreola and Board member Colin Bowkett, allocating free cash flow from the web domain business into promising microcap companies, especially those planning to go from small, high-growth private company status into publicly-traded companies (particularly those needing growth capital investment);

3. SewerVUE, a wholly-owned company providing a multi-technology scan of sewer systems to assess their condition for maintenance prioritization; and

4. A variety of smaller, attractive positions in private and public companies, including an approximately 7% ownership position1 in Alchemy, a now-private company offering the highest quality windshield protection (with a defense technology division as well).

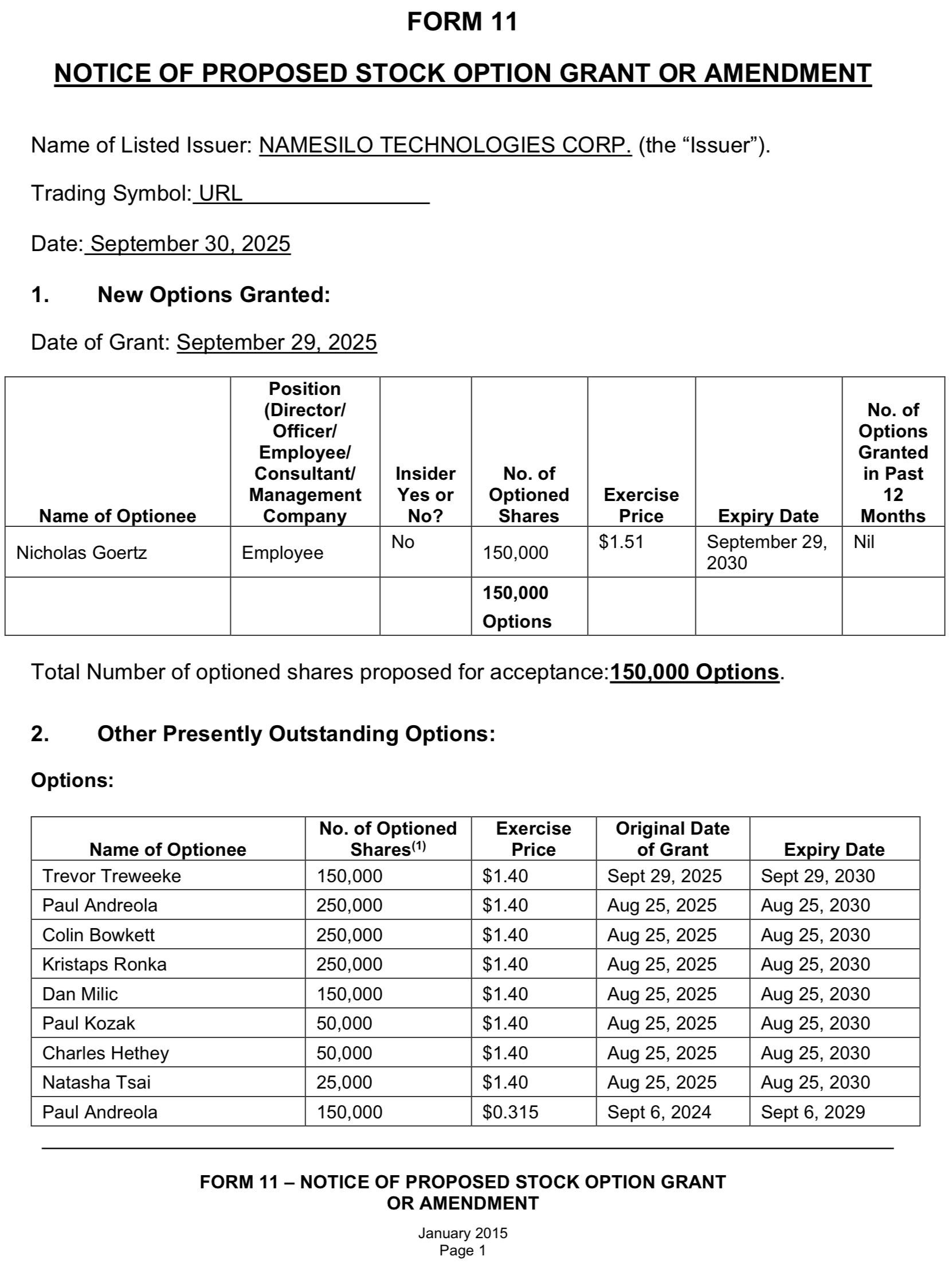

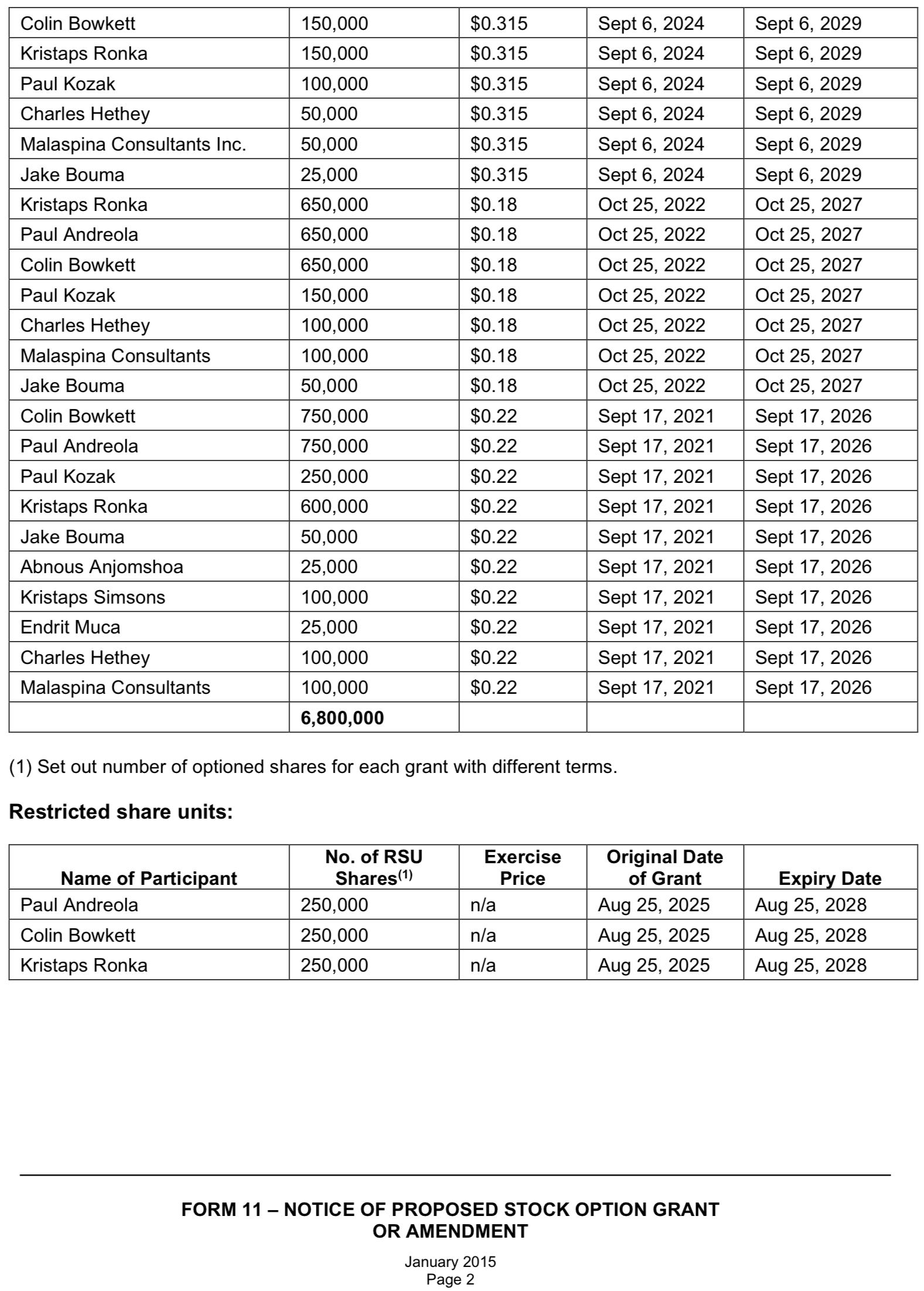

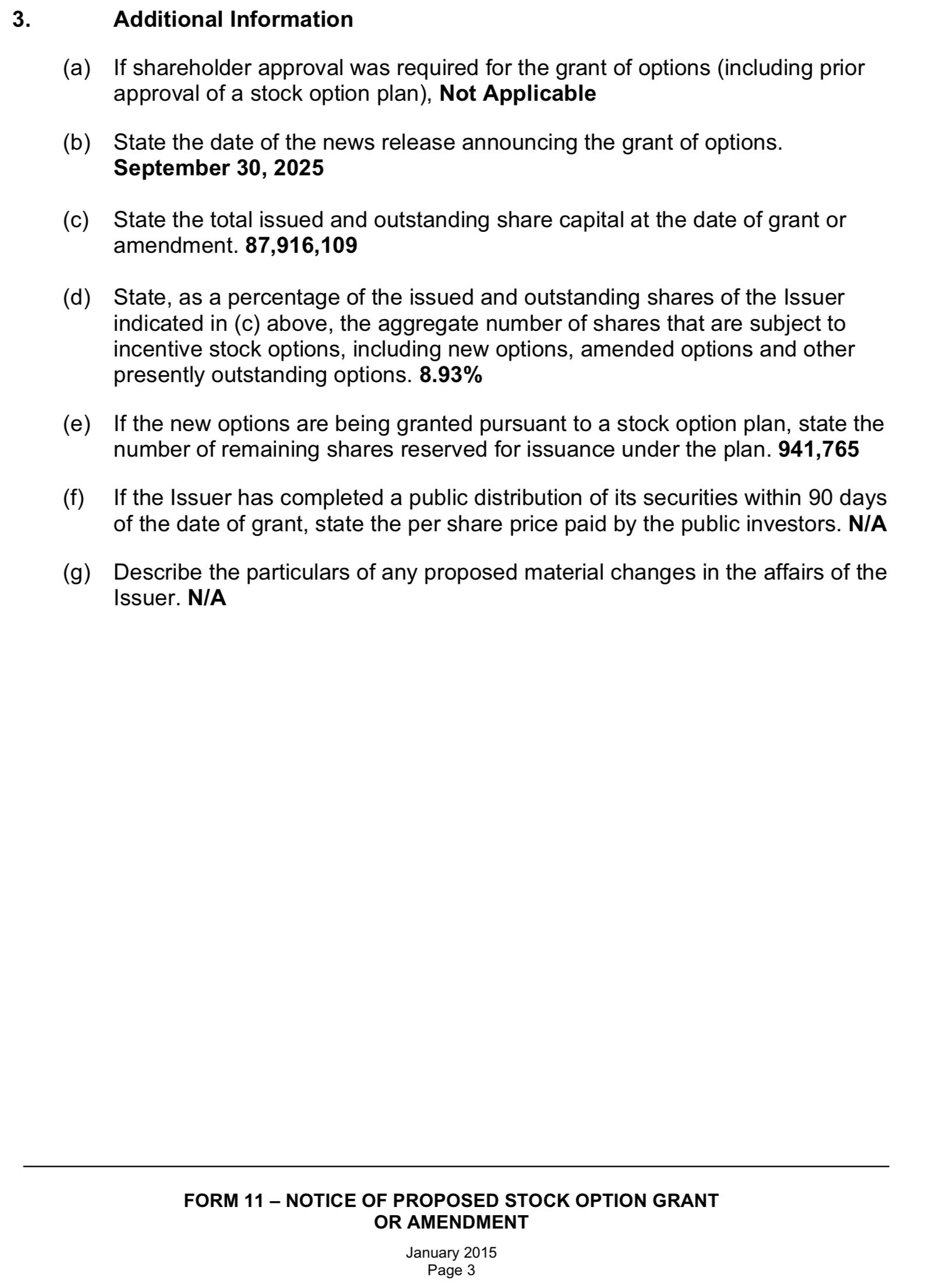

The company’s shares trade on the Canadian Securities Exchange with the ticker URL, and also on the US Over the Counter Market with the ticker URLOF.2 As of September 30, 2025, the total number of issued and outstanding shares were 87,916,109; there were also 6,950,000 outstanding options and 750,000 restricted share units. Appendix A includes the breakdown of those options and RSUs. The remainder of this document will summarize each of the above components and provide some relevant considerations for those considering an investment in the company’s shares. Nothing in this document is investment advice.

1. The web domain business, NameSilo LLC

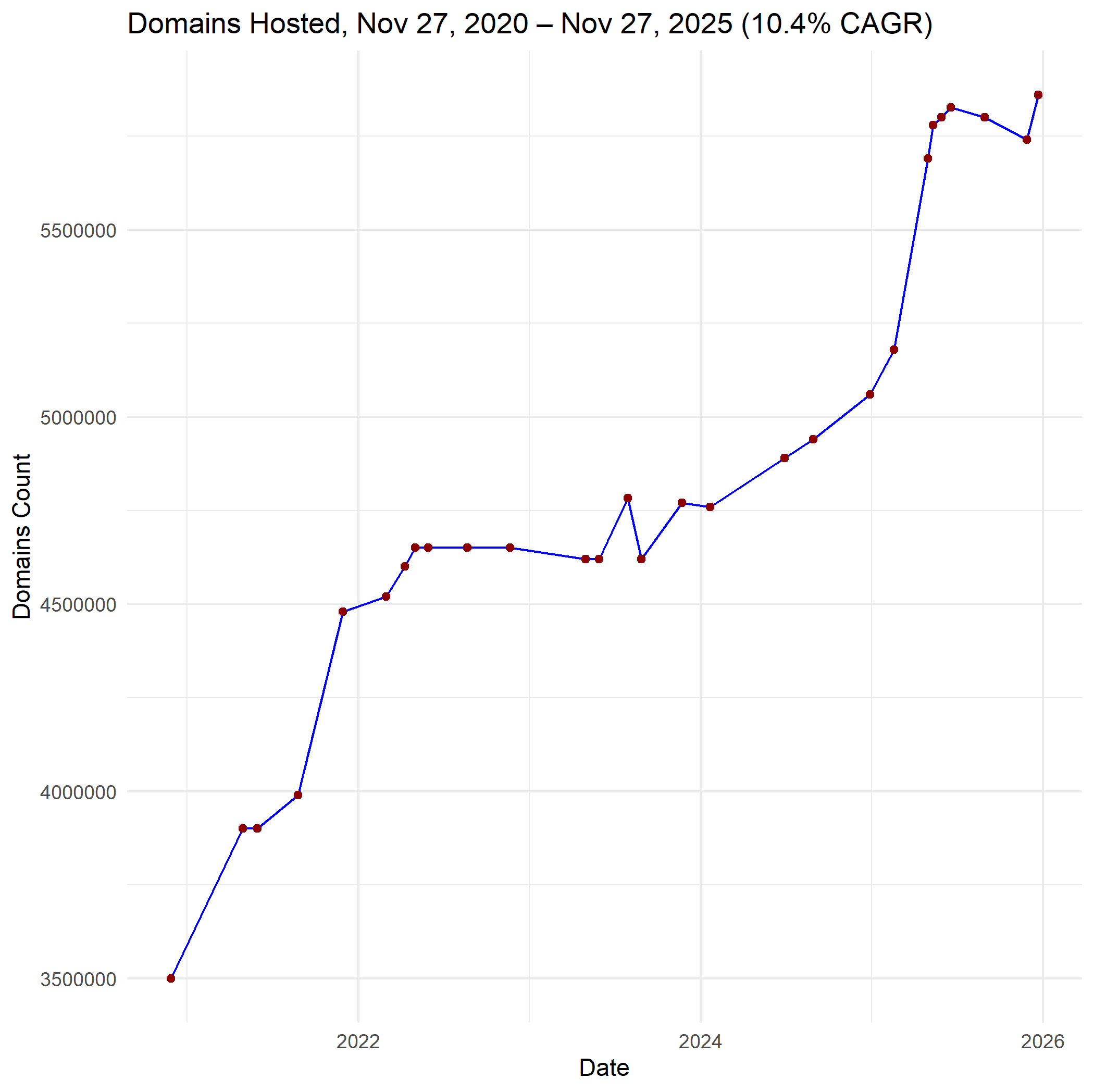

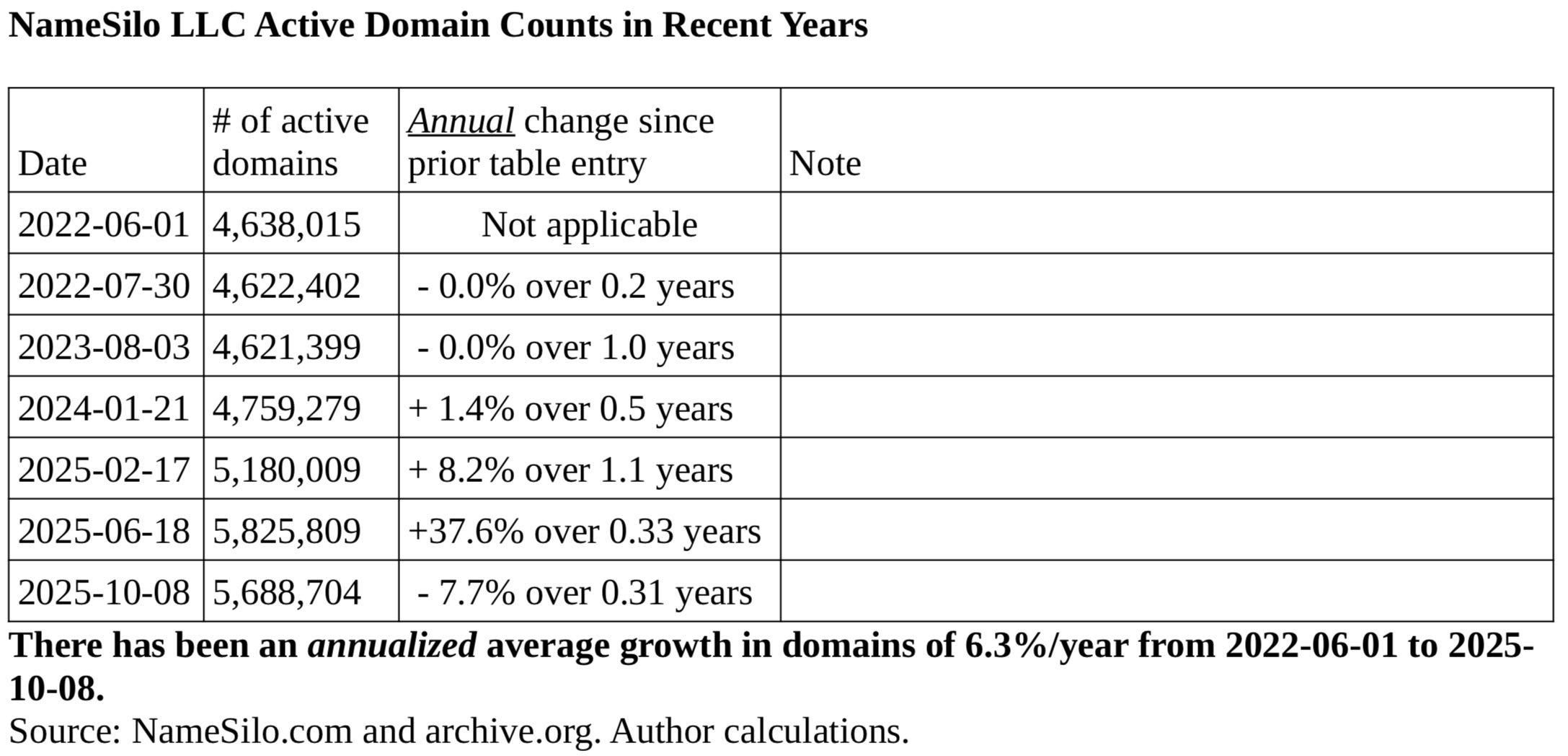

The operating company, NameSilo LLC, is 81.5% owned by the parent company NameSilo Technologies. The web domain hosting business is headed by Kristaps Ronka and hosts approximately 5.7 million web domains.3 The holding company announced the acquisition of its 81.5% position in NameSilo LLC on August 7, 2018, when the operating company hosted ~1.85 million domains.4 The web domain industry is fairly mature, growing at low single-digit percentages annually in recent years. My understanding is that NameSilo is slowly taking market share by offering top quality service at low prices.5 Over the past five years, while the number of shares outstanding has been similar, NameSilo LLC has increased the number of domains hosted by an annualized growth rate of 10.4%, as shown in the figure below.

In addition, NameSilo has added a number of profitable add-on optional services, such as email and security. There aren’t a lot of profitable avenues to reinvest cash flow back into the web domain business, but due to low maintenance capital expenditure needs, free cash flow regularly is dividended up to the parent company, now approximately C$8 million/year,6 where it can be profitably invested in opportunities with a higher expected return. Despite minimal reinvestment opportunities in the web domain business, there have been two recent accretive acquisitions by the operating company, ShortURL in August 2025,7 and a simple web site builder and e-commerce capability in September 2025.8 Appendix B describes my understanding of the trends in the web domain business. Although I am primarily valuing the 81.5% position in NameSilo LLC on its free cash flow generating ability, it’s worth noting that a competitor, NameCheap, was recently bought at a value which values the company at US$1.5 billion; NameCheap currently hosts approximately 11 million domains. While my understanding is that NameCheap generates, on average, around twice as much revenue per domain hosted as NameSilo LLC, and a larger web domain business is likely to generate a higher value per domain, on a per domain basis, 5.7 million domains is approximately half the number of domains of NameCheap. Note that NameSilo Technologies owns 81.5% of the web domain subsidiary NameSilo LLC and currently has a market cap of ~C$133 million (~US$97 million).

2. The Reinvestment Runway

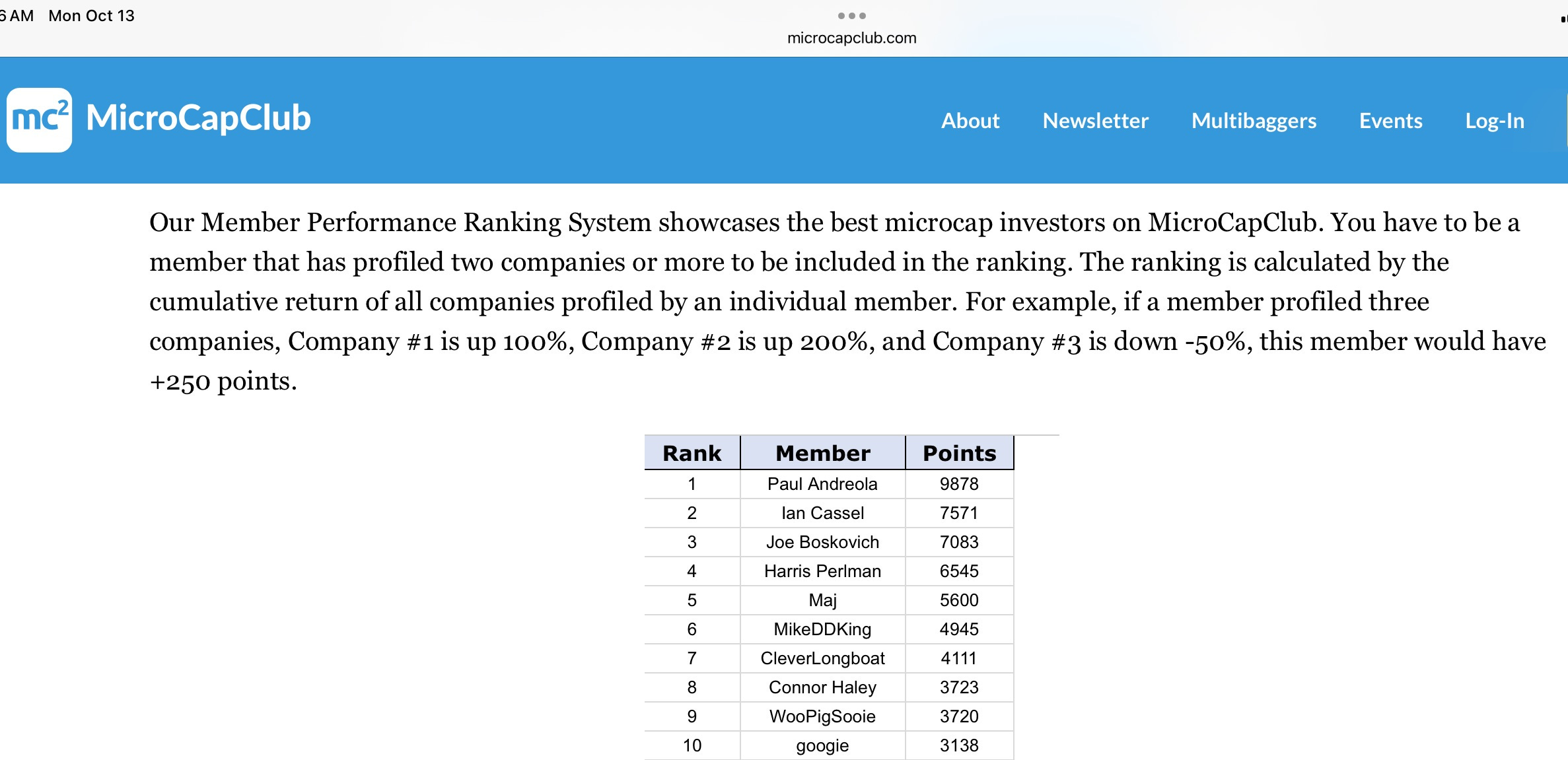

The key to how well the parent company performs over the next several years is how well the parent company reinvests the free cash flow from the web domain subsidiary. In my opinion, the investment process of Paul Andreola is outstanding and promising for the future. He and his colleagues see a great number of investment opportunities. While I believe that process is the most important predictor of future performance, I’ll attach the latest ranking of microcap investors on MicroCapClub.com for another perspective.

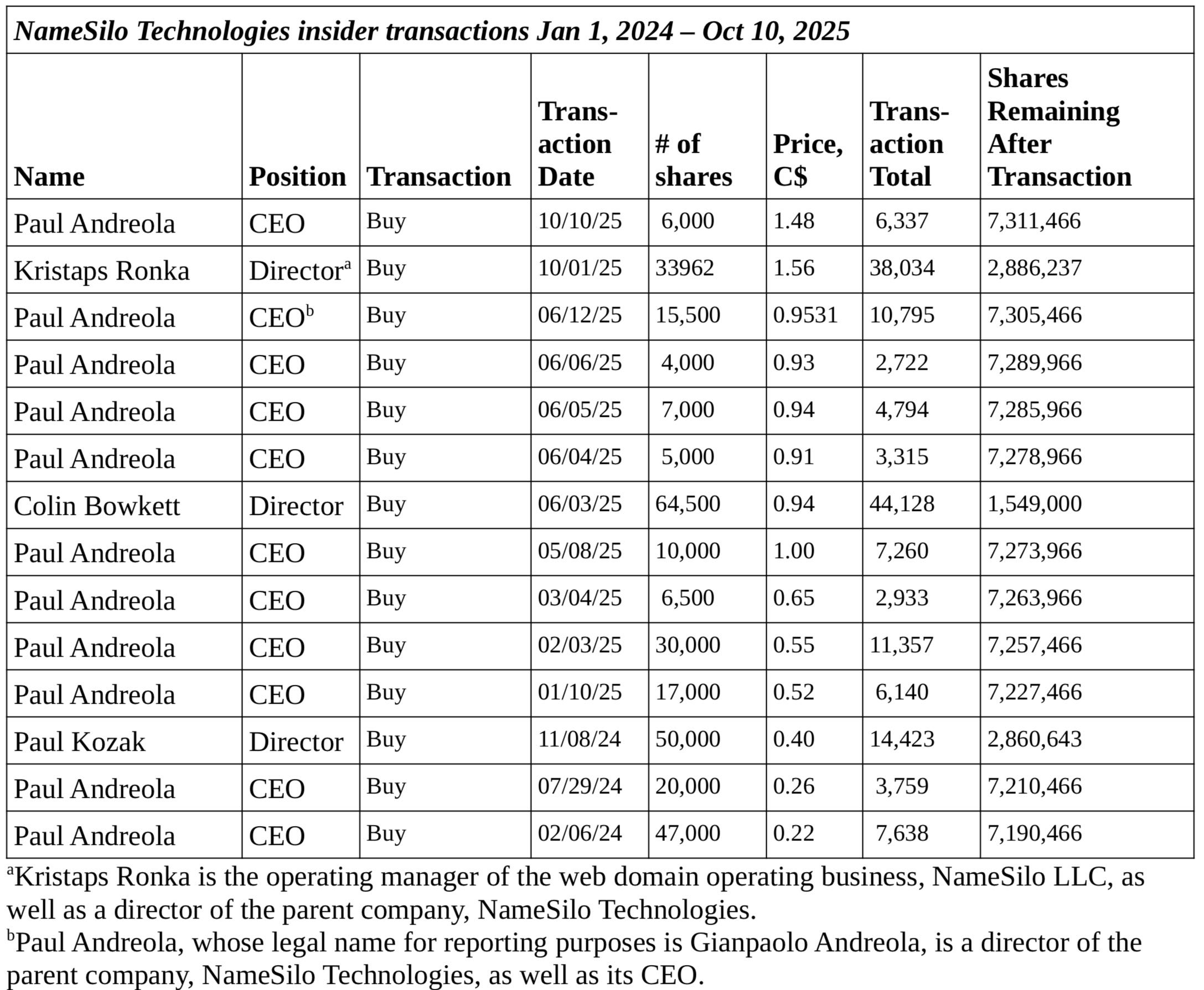

While it appears that the many of management’s shares have been acquired through share options and RSUs, as shown in Appendix A, there have been open market purchases in the past two years:

Thus, it appears that management of the company is aligned with the shareholders at large, although there will be a variety of opinions on whether the extent of share options and RSUs is optimal. Given the excellent investment team and process, and the markets in which they operate, my opinion is that they will be able to achieve at least 20% gross annual investment returns on average.

With the current C$8 million per year of free cash flow sent to the holding company, an analysis needs to consider the costs of operating the holding company. We can look at this two ways: (A) Looking at expenses over the past quarters and comparing that to the incoming estimated C$8 million per year; and (B) Looking at the actual cash coming into the business and subtracting off investments made and change in cash on the balance sheet at the beginning and end of each quarter. Changes in outstanding options and RSUs at the beginning and end of each quarter need to be included.

3. SewerVUE

Most inspections of sanitary sewer condition assessments worldwide are performed by floating a closed-circuit television (CCTV) camera through the sewer. SewerVUE provides the same CCTV camera on the same type of flotation device but also provides Lidar and other technologies to “see” under the water surface and estimate the amount of degeneration of the entire sewer line through acidic gas over the years. SewerVUE is one of the two primary competitors in this space, and NameSilo has the capital to invest in growing this 100%-owned subsidiary worldwide. Two photos of the device are shown, with the device being the one on the left of the poster board; a top view is shown in the photo on the right side. Although the business is currently small, the number of sanitary sewers in the world is large, so there is theoretically potential.

4. Other investments (not operated by NameSilo)

In my opinion, the majority of the NameSilo Technologies investments of free cash flow from the domain business have been very good, especially looking at the “slugging percentage,” that is the returns weighted by the dollar value invested.

For example, Alchemy has what appears to be the world’s best windshield protection product, using nanoparticles to protect the windshield while allowing for visibility and a durable (3+ year) protection. Given the sensors now going through vehicle windshields, the value of this product application could be enormous. The company also has military-defense-related products, but the windshield protection product is likely to be more profitable in a shorter amount of time. NameSilo is likely to have a high-single-digit ownership stake in this private company when it goes public in December 2025 or the first quarter of 2026. The Alchemy stake as well as SewerVUE and the web domain business are likely to be the most profitable parts of NameSilo Technologies in the foreseeable future.

I’m only aggregating the non-SewerVUE, non-web domain hosting investments here since these are likely to be less material to the overall value of the business and share price going forward. Cheelcare (ticker CHER.V and OTC CHCRF) produces a state-of-the-art wheelchair for people with exceptional needs in a growing, global market. Besides having what appears to be the best product on the market, the sales team seems to have strong experience in selling products in their market, and the founders lead an excellent team. Atlas Engineered Products (ticker AEP.V and OTC APEUF) is Canada’s largest producer of roof trusses, floor trusses, and factory-made wall panels. Atlas’s uniquely national scale allows for purchasing and distributions at a lower cost, but the increasing deployment of robotics likely enhances their long-term competitive advantage. Atlas has a strong management team led by their capable founder CEO, solid CFO, and a solid Board. The current total market cap of the company is below replacement cost during the current trough in the Canadian housing cycle. Ola Media is a private company providing a Latin American advertising platform for ride share vehicles and adjacent businesses. Their impressive co-founders have made connections with global advertising agencies and captured a valuable position in Mexico, with promise throughout Latin America. There are other smaller investments, at least most of which seemed sensible to me. Given the growth of the domain business free cash flow in recent years, future investments are likely to be larger than the smaller ones not specifically listed here.

The table below summarizes the ownership stakes in the various businesses THIS TABLE IS STILL UNDER CONSTRUCTION AND SHOULD NOT BE RELIED UPON.

Additional note

The annual report for 2024 and preceding years contains a prominent auditor’s note about the large working capital deficit of NameSilo Technologies and mentions that they are relying on the company for assurances that “going concern” accounting should be used for assessing the financial statements. (See Note 1 of the 2024 annual report, for example.) My understanding of this note is that NameSilo tends to receive payment up front for the web domain services and agrees to provide web domain hosting services for the typically one to ten year period of the contract. NameSilo LLC tends to dividend up some of the cash to the parent company before the contract is completed, where it can be reinvested into more profitable investments than, for example, short-term government bonds. If hugely losing investments were made and the number of new domain contracts were to plummet, in theory the company could become challenged in meeting its obligations. I think that that probability is very low.

Disclosure: I currently own URLOF shares, and I may buy or sell URL.CN or URLOF shares at any time. Nothing in this description or any other statement I make constitutes a recommendation to buy or sell any security, nor is any investment advice whatsoever. You must do your own due diligence or consult a licensed and qualified advisor. I am not your advisor. This description is for educational and entertainment purposes only and may contain unintentional errors or omissions.

APPENDIX A: Structure of NameSilo Technologies Options and RSU grants

APPENDIX B: [To be completed]

ENDNOTES:

From https://investors.namesilo.com [accessed 9 November 2025].

NameSilo Technologies is a Canadian-incorporated public company listed on the Canadian Securities Exchange with the ticker URL, or URL.CN to specify the exchange. It also has a “secondary” listing on the US Over the Counter Market, OTC, with the ticker URLOF. The average daily volume of URL.CN over the past 65 days has been 95,000 shares and the average daily volume of URLOF has been 105,000 shares, as of October 11, 2025. As NameSilo Technologies is “DTC eligible,” URLOF shares can be electronically settled (rather than paper settled in Canada as is the case for some OTC stocks); so URLOF can be traded without commission through Fidelity Investments and possibly other brokers. I trade shares in whichever currency I have available or where it is less expensive at the time.

NameSilo LLC posts the current number of the web domains registered with the company at: https://www.namesilo.com/domain-count As of late October 8, 2025, this was 5,688,704 domains.

The name of the holding company at the time of the NameSilo LLC acquisition was Brisio Innovations. A press release summarizes the transaction.

I gathered reasons for NameSilo gaining market share by an admittedly small amount of market research, mostly reading internet reviews and by comparing pricing and offerings. The number of web domains registered with NameSilo LLC at dates over the past 3+ years available at Archive.org are shown in the table below:

Paul Andreola, September 30, 2025 presentation on NameSilo Technologies at the Small Cap Discoveries 2025 conference, Vancouver, BC, Canada.

ShortURL was acquired by NameSilo LLC in August 2025. ShortURL is likely accretive to earnings as well as allowing NameSilo LLC to cross promote, which should be synergistic without needing to pay for synergy. The press release is available at: https://www.prnewswire.com/news-releases/namesilo-technologies-announces-acquisition-of-shorturl-by-namesilo-llc-appointment-of-new-director-and-grants-of-stock-options-and-restricted-share-units-302538239.html